What the HECM is happening in reverse mortgage lending?!

Continue reading

What the HECM is happening in reverse mortgage lending?!

Continue reading

What can reverse mortgage professionals do today to survive these lean times?

Continue reading

What is the 10-year business cycle and where is our industry in it?

Continue reading

A summary of Reverse Mortgage Daily’s investigation into the causes that contributed to the collapse of Reverse Mortgage Funding

Continue reading

Three factors will shape 2023 reverse mortgage production…

Continue reading

Presently mortgage originators are suspended between uncertainty and the opportunity to innovate our way to…

Continue reading

Since 2009 California has led all states for total HECM endorsements. In fact, according to the Fiscal Year, 2021 Independent Actuarial Review of the Mutual Mortgage Insurance Fund, California accounted for 26% of all HECM endorsements in the fiscal year 2021. Florida, Arizona, Colorado, and Texas trail significantly in endorsements accounting for 7-8% of overall loan volume respectively. California is home to some of the nation’s highest-valued homes and also has seen some of the most rapid growth in Home Price Appreciation. Consequently, any broad declines in home values in the Golden State will have a marked impact on the 2023 and 2024 economic valuation of the HECM Program.

FHA acknowledges this sensitivity in its 2021 report. “HPA is a lagging indicator that tends to overstate

[read more]

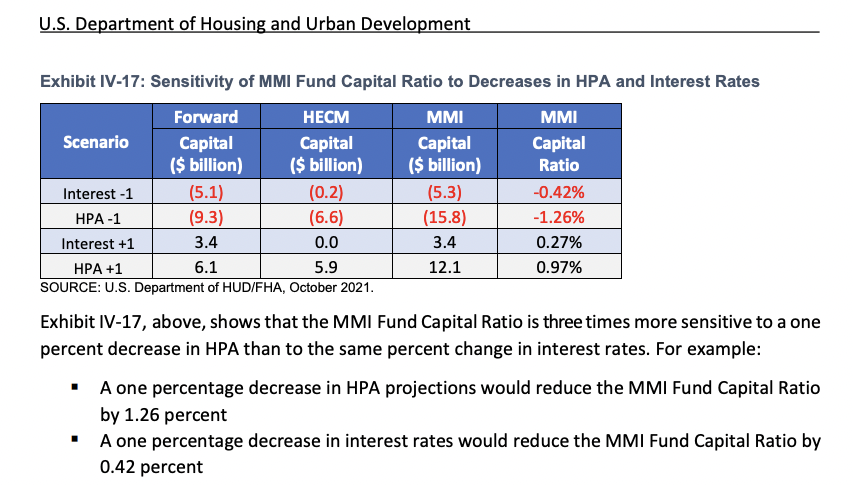

the health of the economy during good times and the weakness of the economy during bad times. Because the MMI Fund Capital Ratio is so closely tied to HPA, the assessment of FHA’s financial health represented by the ratio can change materially and quickly with changes in both actual and projected home values.” The operative word is overstated. To further illustrate this point the Mutual Mortgage Insurance Fund’s capital ratio is three times more sensitive to a one percent drop in home price appreciation than a one percent decrease in interest rates.

the health of the economy during good times and the weakness of the economy during bad times. Because the MMI Fund Capital Ratio is so closely tied to HPA, the assessment of FHA’s financial health represented by the ratio can change materially and quickly with changes in both actual and projected home values.” The operative word is overstated. To further illustrate this point the Mutual Mortgage Insurance Fund’s capital ratio is three times more sensitive to a one percent drop in home price appreciation than a one percent decrease in interest rates.

All of which begs the question, where does the California home market stand today? After a decade of generally consistent gains, home values have turned negative. Zillow reports that home price in Southern California is now 6% below the all-time high reached in May.

For a closer examination, we’ll go to Fortune’s interactive map which shows the markets most likely to see a drop in home prices in the coming year. Markets in dark red are very likely to see home price reductions, those in light pink are rated high, purple is medium, and light blue are the markets less likely to see home price drops. Now moving over to Shasta County California and Redding the county seat, I can see my hometown is very likely to see price drops which I can confirm first hand having seen dozens of listings drop their asking price and closings coming in 10-17% lower. However, we’re not alone with most of the southern California markets also showing a high probability of a fall in home values. Many of these at-risk markets have already seen significant erosion in home values. Between May 2022 and August Shasta county saw values fall by -2.78%, Sacramento values fell by -6.03%,

San Francisco values dropped by -7.8%, and San Jose fell over 10.5%! Los Angeles, Riverside and San Diego also saw values fall.

Looking at metros in other states we can see some of the previous hottest markets poised for a fall. For example, Boise Idaho. The median sales price of single-family homes in the greater Boise area has fallen from a high of $550,000 in May to $510,000-a drop of 8 percent. In the same time period, Reno sale prices also dropped 8% from $625,000 to $580,000. Austin Texas appears to be in a free fall collapsing from a median sales price of $720,000 in May and plummeting to $620,000- a drop of 14% in just three months! If that pace continued Austin prices would fall by 56% year-to-year. It should be noted that two forces have not been factored into this forecast which may accelerate the fall of home values; a recession and continued inflation increasing foreclosure filings.

In conclusion, we’ve been on this journey before; at least those of us who were originating prior to the 2008 housing crash. Whether it’s a coming housing crash or correction our willingness to look at market signals and acknowledge their likely outcome only serves to help us prepare for the future and adjust our mindset and business strategy to succeed. How do you expect California home values will impact reverse mortgage lending? Let us know in the comment section below.

Redfin Monthly Housing Market Data (Charts shown in video)

2021 FHA Annual Report to Congress

Odds of falling home prices in your local housing market, as told by one interactive map

Rising mortgage rates are sending home prices lower

[/read]

![]()

The following originally appeared in HECMWorld in September 2020

“I’ll take my family on a nice vacation once I make enough money.”“I’m going to create a killer marketing plan that will attract more homeowners and help me close more loans.”

These are just a few examples of the rationalizations for why we’re doing things the way we are and avoiding the work required to reach our goals.

You may not have the money for a family cruise, but you may be able to take your family on a weekend getaway and not break the budget in the process. An imperfect business plan is better than nothing. Why not put pencil to paper and begin with a rough outline?

Truth be told, it’s the little things that often yield the best results. Taking 15 minutes without distractions to sit with your partner, child, or colleague to ‘check-in’ maybe ‘just one more thing’ but it may be the most important thing for them that day. Our lives have an overabundance of ‘just one more thing’ to do. The trick is to confront our tasks as if they were the last thing we will do.

What’s most important at this very moment? Taking a moment to give a sincere compliment? Inviting over your friend who’s overwhelmed to simply sit and relax in your backyard? Calling your widowed borrower to see how they’re faring during the pandemic? Is it shutting down your email and silencing your cell phone to make 15 outbound sales calls?

Each of us knows what that ‘just one more thing’ is. The question is what will we do without for the moment to make it happen?

As the housing market goes, so does the HECM. One real estate economist makes these predictions for 2022.

Continue reading

“We are considering some other changes [to the HECM program]”. Those are the words of FHA Commissioner Brian Montgomery during a media conference call for the release of FHA’s report to Congress last week. “I don’t think we ever envisioned that the FHA reverse mortgage product would dominate the market, for now, almost 30 years. I know there have been some proprietary products that have grown in the industry.”

It was in fact 32 years ago that Congress passed a bill creating a pilot program of the Home Equity Conversion Mortgage. As it’s said, ‘the rest is history’. That history shows us subdued HECM loan volumes until 2002 when endorsements broke 10,000 units for the first time and then skyrocketed seven short years later to a staggering 114,000+ loans.

Did Congress anticipate that the federally-insured reverse mortgage would consistently represent over 90% of the market? Most likely not. In the last decade, both HUD and FHA officials have expressed their desire for an expansion of the private market and less reliance on FHA. In the years leading up to the housing crash of 2008, there were a handful of popular private reverse mortgage options on the market. While primarily popular with homeowners with values that exceeded FHA’s lending limit they did not significantly shift new applicants with moderate home values away from the HECM program.

Traditionally private or proprietary reverse mortgages have been confined to homes that appraised above the national lending limit. Recently, however, a few select lenders have broadened their product offerings- one to include properties valued as low as $400,000. This could entice potential borrowers who wish to avoid the significant upfront and ongoing costs that come with FHA mortgage insurance premiums.

What would possibly attract more homeowners to a private reverse mortgage solution? Here are just a few existing and potential features that are appealing.

Despite the incredible potential of private reverse mortgage loans the HECM continues to attract the lion’s share of older homeowners. As long as housing market conditions remain ideal expect to see more innovative private products that may move us toward a more diversified market.