Despite the Federal Reserves rate hikes inflation has begun to surge. A look at the underlying factors that continue to push up the cost of living…

Continue reading

Despite the Federal Reserves rate hikes inflation has begun to surge. A look at the underlying factors that continue to push up the cost of living…

Continue reading

Sandwiched between the Millennials and Boomers Generation Xers who are poised to become the next reverse mortgage market.

Continue reading

Industry expert, author, and founder of Understanding Reverse contributed a column to Housing Wire’s Reverse Mortgage Daily that reveals two often overlooked facts about the HECM’s expected rate used to determine the federally insured reverse mortgage’s principal limit.

Continue reading

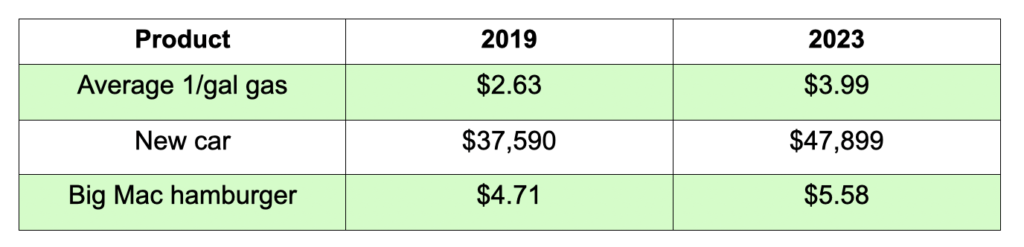

There’s one conversation that every financial advisor should have with their clients. A conversation that should also be explored by reverse mortgage professionals with every potential borrower. Inflation. Questions such as “How are you coping with the higher price of everyday goods and services you’re paying today?” can reveal a cashflow crunch that needs to be addressed.

Continue reading

Here’s why Americans can no longer ignore their economic pain…

Continue reading

The risk of ‘Fiscal Dominance’ and how it would shape reverse mortgage lending…

Continue reading

Despite holding trillions of dollars in home equity, U.S. homeowners are struggling to tap into it according to a report published by Point, an alternative equity release company.

Continue reading

Here are the five signs of an impending recession, 4 which we’ve already seen.

Continue reading

The curse of money printing has put pressure on the 10-year CMT and consumer interest rates…

Continue reading