Stalled home prices are making the Federal Reserve’s task of reducing inflation much more difficult. See the Chairman’s recent comments on the housing market and what actions the Fed may take…

Continue reading

Stalled home prices are making the Federal Reserve’s task of reducing inflation much more difficult. See the Chairman’s recent comments on the housing market and what actions the Fed may take…

Continue reading

Older homeowners in financial distress may have overlooked the ultimate pick-a-pay loan.

Continue reading

Soon credit may be unavailable to millions of Americans. What can older homeowners do?

Continue reading

Retirees have many reasons to be anxious. Here are 5 Fears older homeowners often face and potential solutions.

Continue reading

These are the consequences retirees now face in the midst of a manufactured recession…

Continue reading

Unable to use the embedded player? Listen here.

[Reverse Mortgage Daily] In RMD’s most recent podcast Chris Clow interviews one originator who’s found what he sees as the most effective approach to reverse mortgage communication.

.

Other Stories:

Protect Your Retirement Income from Inflation

[Fortune] ‘Poison’ Ivy Zelman—the analyst who predicted the 2008 housing bust—sees U.S. home prices falling in both 2023 and 2024. Here’s how much

Now is the time for homeowners, financial professionals, and mortgage brokers to put aside notions based on bias and instead embrace the reality that most retirees are facing at this present moment

Continue reading

Stagflation is a particularly ugly word for those old enough to remember the brutal effects of high inflation and high unemployment in the 1970s. And speaking of inflation if we measure it by the same basket of goods used in the late 70s and 80s the annual inflation rate would be 15%, Apparently, inflation is neither 8.5% nor transitory. With inflation surging as the economy stagnates concerns of stagflation have returned. Stagflation, the dreaded S-word of the 1970s or what some economists call the bitterest of economic pills.

However, all is not lost. What we are witnessing is an economic cycle, one that reminds us that every bill eventually comes due. A bill for decades of government largesse, easy money, and trillions of dollars in Covid stimulus. Ironically, the pandemic didn’t crush our economy but our response to it will harm millions of Americans. Today we are just beginning to see the outcome of central bank policies and political will. Both stand to especially harm those who are retired and living on a fixed income.

And speaking of a fixed income, often the image of a poor miserly penny-pinching pensioner often comes to mind. But, truth be told, a retiree bringing in precisely $60,000 a year is just as much on a fixed income as the one earning $90,000. Beyond their income disparity, each will feel the brunt of inflation differently; what some financial planners call their individual inflation rate. For example, a 70-year-old widower who’s renting is exposed to more inflationary pressures with rising rents than a 70-year-old who’s living in a home with a fixed mortgage payment. Yet both are experiencing consumer price inflation in non-discretionary items such as gasoline, food, prescriptions, electricity, natural gas, and heating fuel.

So where does this leave future reverse mortgage applicants? In short, they’ll need to have considerably more equity accumulated to offset the impact of higher interest rates and the subsequent lower principal limit factors that determine how much money for which they may qualify. I say considerably because an effective interest rate of 7.5-8.5% for a HECM loan is not far-fetched. And, keep in mind in the years 2005-2007 during the heydays of HECM lending, the average expected rate hovered just below seven percent. Certainly, the presence of large retail banks originating HECMs helped, but the pool of eligible homeowners with adequate equity was there and remains today.

Looking back to interest rates keep in mind that the Federal Reserve has only just begun to throw cold water on inflation by increasing interest rates to slow the economy. Rates that many economists say must be higher than the rate of inflation to be effective. If true, this leaves much headroom for future rate hikes unless inflation shows early signs of retreating or unemployment begins to spike.

Granted, entering a period of inflation, economic contraction, and possible stagflation is somewhat unnerving. However, it is during these times of upheaval that economic solutions, such as reverse mortgages may regain their luster and appeal. After all, where else will older homeowners find the additional ten, fifteen, or twenty percent additional cash flow to offset the increased cost of living?

The pieces are now falling into place. Consumer spending has dropped considerably. Large ticket items and even housing could see deflation. Inflation is crushing consumers who are now cutting back on discretionary spending. Last week the nation’s two largest retailers Walmart and Target reported massive drops in profits. Target alone shed 25% of its stock value last week after reporting a stunning 52% drop in profits. CNN Business reports Target was also forced to write down the value of excess inventory that’s just sitting in warehouses. In other words, consumers are on strike only buying necessities.

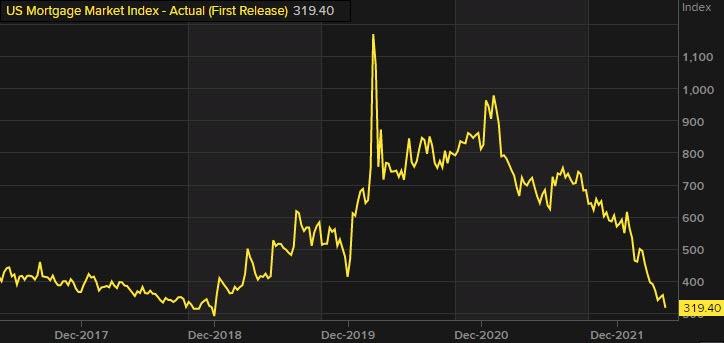

Traditional mortgage lending is feeling the full force of economic forces that have returned to roost after a decades-long absence; inflation and rising interest rates.

On the supply side…

Sure. The speculation is rampant and varies widely among housing market ‘experts’ and economists. But are today’s housing prices really sustainable?

Continue reading