FHA Commissioner Julia Gordon reaffirmed the agency’s commitment to the HECM program in her keynote address to the National Reverse Mortgage Lenders Association (NRMLA) Annual Meeting in Nashville, Tenn last week.

Continue reading

FHA Commissioner Julia Gordon reaffirmed the agency’s commitment to the HECM program in her keynote address to the National Reverse Mortgage Lenders Association (NRMLA) Annual Meeting in Nashville, Tenn last week.

Continue reading

A crisis of housing affordability is pushing many would-be homebuyers to the sidelines. One solution may help…

Continue reading

Unable to use the embedded player? Listen here.

Just how is the HECM for Purchase performing? That’s a question that RMD addressed last week sharing the perspectives of several industry lenders.

Reverse Market Insight’s Market Minute

The housing boom could be losing steam

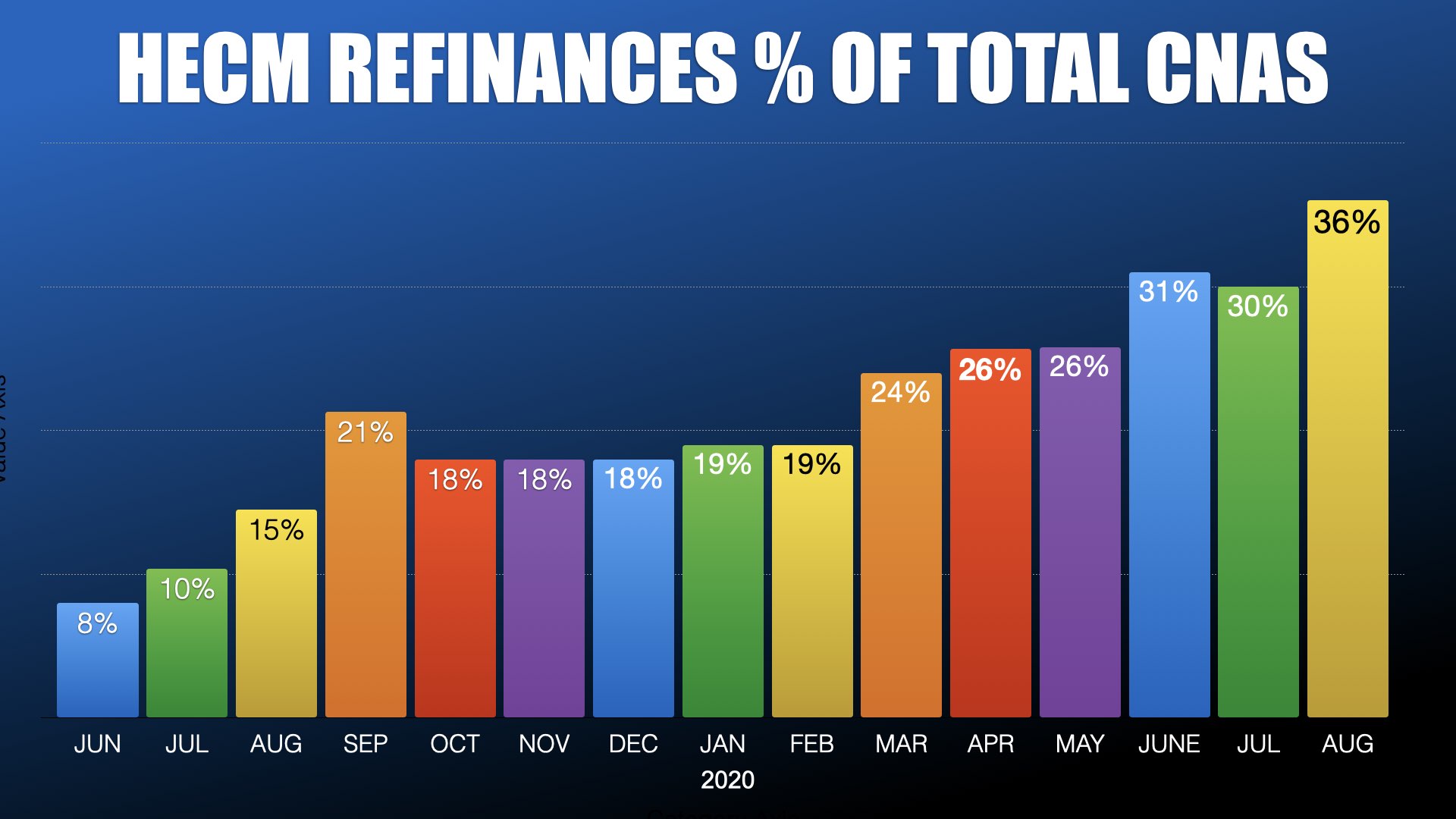

The Federal Reserve’s interest rate cuts and government economic stimulus have given our economy a pure sugar rush. One of the early manifestations of this ‘sugar high’ can be found in the mortgage market’s surge of refinancing activity.

Traditional mortgage refinances are 50% higher than a year ago according to the Mortgage Bankers Association. Home Equity Conversion Mortgage refinance transactions also climbed from an average of 5.4% in 2019 to an average of 20% of all FHA case numbers issued for the federally-insured reverse mortgage. In fact, August set a new high for refinance activity with 36% of all HECM case numbers being HECM-to-HECM refis transactions.

Against this backdrop fiscal year 2020 endorsements for the HECM grew 34% over 2019. A considerable part of that increase can be attributed to this new yet anticipated spike in HECM refinance activity.

[read more]

While traditional borrowers are reducing their monthly payment by hundreds of dollars, those refinancing a HECM are harvesting additional cash thanks to their home’s value and record low interest rates.

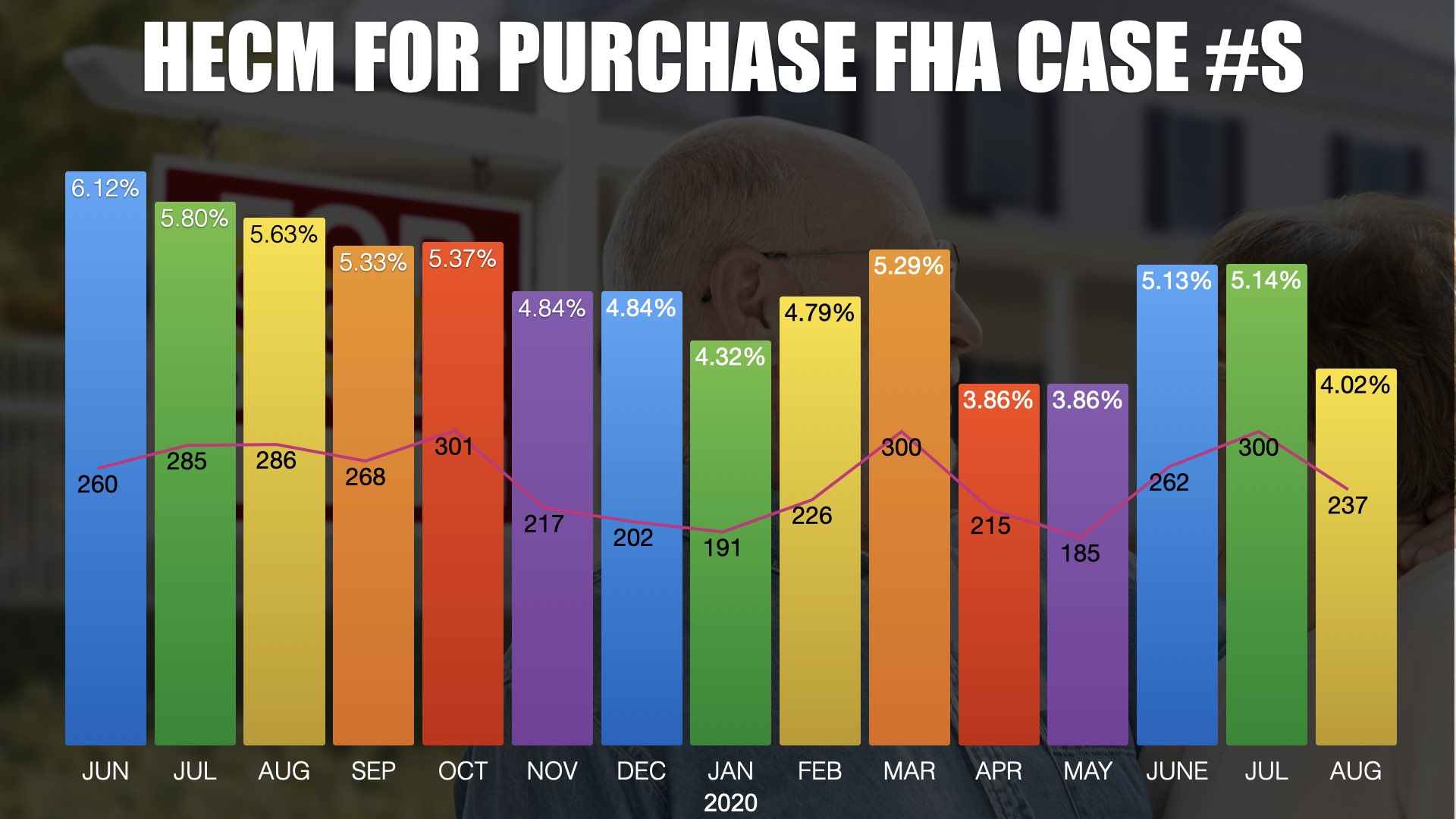

All with all cycles, they eventually end. Where will originators turn once the refinance boom fueled by low rates fades? One market that still holds potential but has yet to see significant growth are HECM purchase transactions. Since June 2019 H4P (HECM for Purchase) case numbers have hovered between a modest four to six percent of application case numbers assigned by FHA.

While the H4P market certainly requires ‘a particular set of skills’ to work closely with realtors and a solid understanding of sales transactions, originators still can make significant inroads. With real estate values peaking buyers can sell their home at a record price and make a much smaller down-payment thanks to effective interest rates between three and four percent. However, buyers face the challenge of a housing inventory shortage.

Existing home sales hit a 14-year high but not enough new homes are being built to meet demand. Last month Bloomberg reported that home inventories would be exhausted in three months at our current pace of existing home sales. Not surprising considering the impact the COVID-19 pandemic shutdowns had on new construction labor, materials manufacturing, and financing disruptions. Housing inventory is expected to increase appreciably next year when mortgage and eviction forbearance measures end and new home construction projects are completed.

The outcomes of economic stimulus can be seen in all segments of the U.S. economy. Preparing for the next phase of HECM marketing and production is vital for success as we face the economic uncertainty of a second wave of the coronavirus and enter the new year.

[/read]

The HECM for Purchase provides you with unique opportunities to open up the conversation about…

The HECM for Purchase provides you with unique opportunities to open up the conversation about…

About John Luddy: John has trained reverse mortgage professionals how to be successful when sitting face-to-face at the kitchen table with prospective HECM borrowers. Norcom is looking for qualified loan officer candidates. To learn more call 1-860-507-2582 or email John Luddy here

“Failing to provide a client with viable options can be just as damaging, if not worse than providing poor advice”

Such is the case in a recent post I read on LinkedIn from Florian Steciuch. He wrote “ My definition of heartbreak – meeting with an 82 year old client who was given a 30 year mortgage when she bought her new town home last year. Recently she lost her part-time job, now has Social Security of [sic] $1300 with a mortgage P+I of $700. She already missed her property tax payment. She provided a down payment of 50% – this is a prime example of why the FHA HECM for Purchase was a far superior loan option. She would have had NO mortgage payment. She was not offered this option because her bank did not offer it. 80 year old home owners should not be taking on the risk of 360 months of mortgage payments if they have a substantial down payment.”

Such is the case in a recent post I read on LinkedIn from Florian Steciuch. He wrote “ My definition of heartbreak – meeting with an 82 year old client who was given a 30 year mortgage when she bought her new town home last year. Recently she lost her part-time job, now has Social Security of [sic] $1300 with a mortgage P+I of $700. She already missed her property tax payment. She provided a down payment of 50% – this is a prime example of why the FHA HECM for Purchase was a far superior loan option. She would have had NO mortgage payment. She was not offered this option because her bank did not offer it. 80 year old home owners should not be taking on the risk of 360 months of mortgage payments if they have a substantial down payment.”

Perhaps this 82 year old would have averted disaster had she read an article similar to Jack Guttentag’s, aka ‘The Mortgage Professor’ latest contribution in the Huffington Post, “Purchasing a House with a HECM Reverse Mortgage: How to Do It Right”. Guttentag opens stating “Purchasing a house with a HECM reverse mortgage has the great advantage that it does not impose a monthly payment burden on the borrower.”