HECM borrowers with loans serviced by RMS have questions after receiving bankruptcy notices from Ditech

The financial woes of Ditech have been documented in recent months. The parent company of RMS (Reverse Mortgage Solutions) is sending out required notices of Ditech’s bankruptcy proceedings which have triggered concerns for many borrowers.

We received the following contribution from Tim Linger HECM Senior Home Financing which spells out what borrowers with loans serviced by RMS need to know.

Submitted by Tim Linger

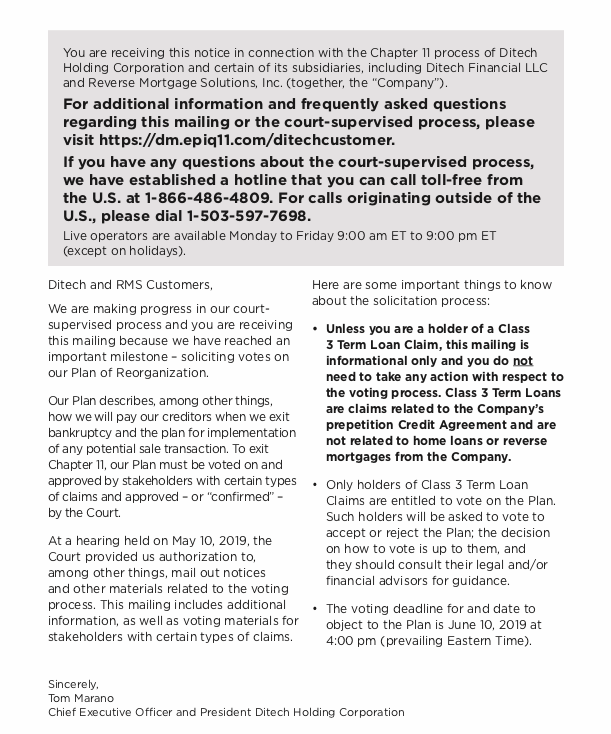

Borrowers with HECM loans serviced by Reverse Mortgage Solutions (RMS) are receiving  letters indicating the bankruptcy filing of Ditech, a parent company of RMS. As you can imagine, borrowers are concerned.

letters indicating the bankruptcy filing of Ditech, a parent company of RMS. As you can imagine, borrowers are concerned.

HECM loan servicing is an important part of the overall HECM process. Reverse mortgage loans stay in this final stage of servicing for the majority of their existence. The other loan stages such as origination, processing, underwriting, closing, and funding, are rather brief in comparison to the servicing period.

The originating broker or initial lender may or may not be the servicer of the HECM loan. In all likelihood, the loan’s servicing rights may be transferred between servicers during the life of the loan and perhaps, even assigned to HUD’s contract servicer before the loan is ultimately terminated.

The servicing company is important to the borrower(s) because their servicer is the central point of contact when questions arise about their loan.

What happens when the servicer ceases operations or no longer services the HECM per the original loan contract? The answer is, per HUD’s guarantee, even though the loan servicer may change, the terms of the HECM remain the same.

You see, the rules of reverse mortgages are determined by the written promises made by the lender to the borrower(s) in the legal closing documents (Note, Deed of Trust and Security Agreement) that the borrower(s) signed at the closing of the HECM.

Regardless of who services the HECM, the borrower(s) can only require those specific items agreed upon in the initial legal documents signed at closing. FHA insures the HECM and therefore, guarantees that no matter may happen to the Servicer, the borrower(s) continues to have a safe and valid contract.

The two common questions from Borrower(s) are: ‘is my HECM safe and, ‘what do I need to do?

First, don’t panic. The purpose of FHA’s Mortgage Insurance Premium (MIP) should give all Borrower(s) full faith that the full faith of the federal government (FHA / HUD), is backing the HECM program and the terms of the loan. The servicer is ultimately communicating what FHA has promised and their guarantees are solid – as solid as the federal government. Yes, the HECM is safe.

Second; What do I need to do? Nothing, unless the borrower(s) feel they have a claim to file. Rest assured that FHA is on the case! HUD guarantees that the loan will be serviced properly, or that the servicing rights would be transferred to another servicing company. Monthly statements, loan proceeds, lines of credit, additional fees, and all terms of the contract will not be affected or changed by any entity, including RMS or it’s parent company’s (Ditech) bankruptcy filing. Sit tight and relax, everything is going to be alright.

Written by Tim Linger, CHS, CRMP, CSA, President of the HECM Association

Tim Linger is a Certified HECM Specialist, Certified Reverse Mortgage Professional, Certified Senior Advisor, and the President of the HECM Association – a 501(c)3 non-profit trade association. Tim has nearly 20 years exclusively in the reverse mortgage arena and prides himself on knowing the HECM thoroughly. Tim is based in Orlando Florida and is the owner of HECM Senior Home Financing Inc. His brokerage focuses on the HECM for Home Purchase. Tim can be reached at TimLinger@HECMsenior.com or direct at 321-356-9229