Today reverse mortgage lenders and originators face a complex trifecta of headwinds that have curtailed HECM loan production and qualified applicants. However, recent data may hint at a modest turnaround. Regardless, a brief review of milestones that helped shape reverse mortgage loan production may provide context for today’s marketplace.

A brief history of reverse mortgage lending

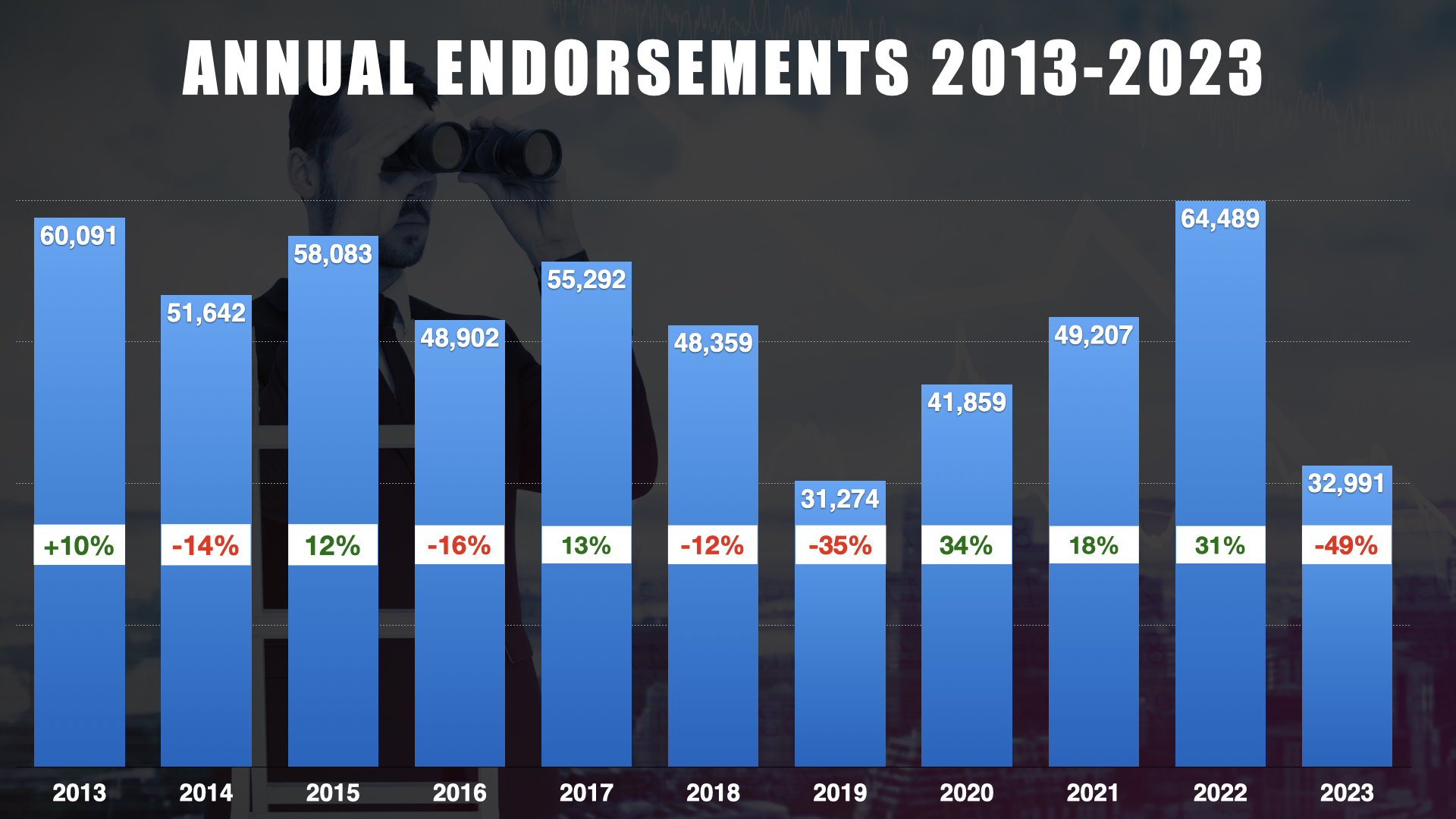

In the wake of the Global Financial Crisis (GFC) of 2008 HECM loan production began to fall precipitously from its peak of 114,692 endorsements in fiscal year 2009. The following year began to reveal the impact of falling home values as endorsements fell 31% to just over 79,000 units.

By 2012 HECM endorsements had fallen to 54K units or nearly half of 2009’s high-water mark. Not surprising considering that Wells Fargo, at that time the industry’s largest reverse mortgage lender, exited the space in 2011 and accounted for 26% of all HECM endorsements. That same year Bank of America ceased their reverse mortgage operations.

The loss of the industry’s two national brand distribution channels was a game-changer.

2013 brought the watershed legislation known as the Reverse Mortgage Stabilization Act. The reforms while improving consumer protections also restricted the number of homeowners who may have been previously eligible for the loan. A series of cuts in the principal limit factors that determine how much money a borrower may qualify for based on age and the effective interest rate also left many would-be borrowers short to close.

By 2015, the Financial Assessment began to require borrowers to show they had the financial capacity and willingness to stay current on their property charges making them less likely to face a technical default. From 2012 to 2018 HECM endorsements ranged anywhere from 48,000 to 60,000 units, that is until 2019 when only 31,000 HECMs were endorsed. Little did we know that help was on the way courtesy of the Federal Reserve.

The pandemic boom & bust

March 2020 saw a novel virus bring the world economy to a halt. Few could have ever imagined reverse mortgage loan volume was about to surge.

After a series of modest cuts to the Fed Funds Rate, in March 2020 the Federal Reserve began slashing its benchmark inter-bank lending rate from 1.5% to nearly zero as a worldwide pandemic took hold. With an economy awash with cheap money and trillions of dollars in stimulus home values climbed at a historic pace.

Consequently, previous reverse mortgage borrowers found themselves with ample equity to harvest more of their home’s value with a HECM-to-HECM refinance. In fact, at the height of the HECM refinance boom refis accounted for half of all HECM endorsement volume.

Of course, what the Fed gives the Fed can take away thanks to inflation. Seeing a record surge in consumer spending and prices the central bank began a series of incremental and increasingly severe rate hikes in March 2022 after two years of easy money and low rates.

Naturally, reverse mortgage refinances became increasingly difficult to find, and loan volumes fell from over 64,000 endorsements in 2022 to nearly 33,000 the following fiscal year.

{kind=link}

1 Comment

These are valid concepts that should not be taken lightly; however, I am a numbers guy who hears well thought out positions but is full of doubts when the numbers do not positively correlate with the an optimistic outlook. Shannon presents the historical perspective well.

.

Where Shannon and I differ is in the near term picture. I have little doubt that HECM endorsement volume will continue its downward trend. The second calendar quarter of 2023 fell to 6,576 HECM endorsements from 8,460 HECM endorsements in the first quarter of that year. Then in the third quarter total HECM endorsements climbed to 8,346 only to fall to 7,114 during the last quarter of 2023 and even further in the first quarter of this calendar year all the way to 6,111. Based on 1) the four month lag rule, 2) the total case numbers assigned in the three month period ended February 29, 2024, and 3) the modified and annualized conversion rate through February 29, 2024, it does not appear that the HECM endorsement count for the second calendar quarter of 2024 will be about 5,900. If that is the case and without the case number assignment count through May 31 2023, I would be merely guessing as to the most likely endorsement count for the third calendar quarter of 2023.

.

While my short term view is very much restricted by the three factors above, my long-term view is less so since the most reliable measure is based on less reliable trend analysis. Like most of you, as to the third quarter of 2024, I hope Shannon’s view prevails.