Some say the current U.S. housing market is a dead man walking. That’s understandable as the Federal Reserve’s repeated interest rate hikes have destroyed buyer demand and pushed affordability out of reach for most homebuyers. But what about today’s potential reverse mortgage borrower? That depends on three factors to name a few.

Higher rates vs. higher home values

While the median home sale prices have fallen significantly in serval U.S. metros, the vast majority of homeowners who’ve owned their home at least four years have seen their home value surge thanks to the pandemic-driven, FOMO-motivated, and Fed-created housing bubble. Was it normal and sustainable growth? No, but it has provided an equity cushion millions of older homeowners did not have three short years ago.

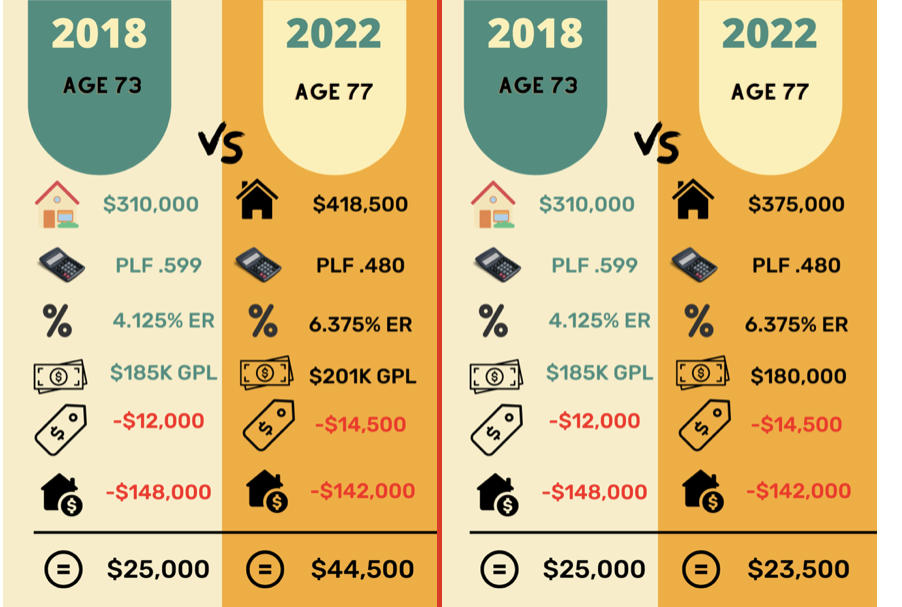

U.S. Homes appreciated by 43% on average between 2019-2021. That means a home worth $310,000 in 2018 could be worth as much as $443,000 this year. For the sake of argument, let’s say the home only appreciated 21% during the same time period. The home’s value still would have grown by $65,000 to $375,000. While despite being three years older the higher interest rate reduced the homeowner’s principal limit factor, yet the gross loan proceeds before fees and payoffs are only $5,000 less than they were in 2018.

The bottom line is unless the homeowner has a high outstanding mortgage balance that exceeds 45-50% of the home value, they may qualify. And that is the crux of the matter: finding homeowners with a lower mortgage balance. Where can one look?

One possibility is to partner with a local mortgage broker who’s looking to diversify its product offerings. After all, mortgage purchase applications are down 42% from one year ago.

Another potential source is mortgage lead providers who may be able to provide age-eligible leads with lower outstanding LTV ratios.

Public workshops are another potential source of qualified leads. You may be able to attract ideal candidates by promoting the question ‘is my equity safe in today’s market’ or similar headlines.

There’s no single remedy for attracting more potential borrowers, yet knowing the potential despite an ugly housing market may give one the motivation to put in the work to find creative lead sources.

1 Comment

Great points. We should look at this with a glass half full perspective.

There’s lots of people out there we can still help.