These are challenging times for reverse mortgage originators and our traditional mortgage counterparts. Rapidly rising interest rates have reduced potential loan proceeds or purchasing power, and HECM-to-HECM refinances have dwindled to a trickle. In such times it’s not uncommon for one to feel the window of opportunity has closed but has it?

[read more]

For some, it has, for others it has not.

Exhibit 1: Potential borrowers who may have qualified last year with enough money to eliminate their existing mortgage and pocket a little money are in for a rude awakening. And those who had little or no mortgage balance may qualify may feel the loan has lost its appeal. Brenda Grauer, a reverse mortgage counselor with Housing Options Provided for the Elderly (HOPE) spoke with Reverse Mortgage Daily earlier this month and recounted her story. Last year in doing the calculation for a couple, the gross loan proceeds before fees and insurance would have been approximately $162.600 on a $300,000 home. Twelve months later that same couple would only get about $127,000 or a 28% percent reduction in funds.

It’s true. Prospective borrowers with significant mortgage payoffs who decided against the loan in 2021 are more likely not to have the equity required to qualify. However, when it comes to the housing market, timing is everything.

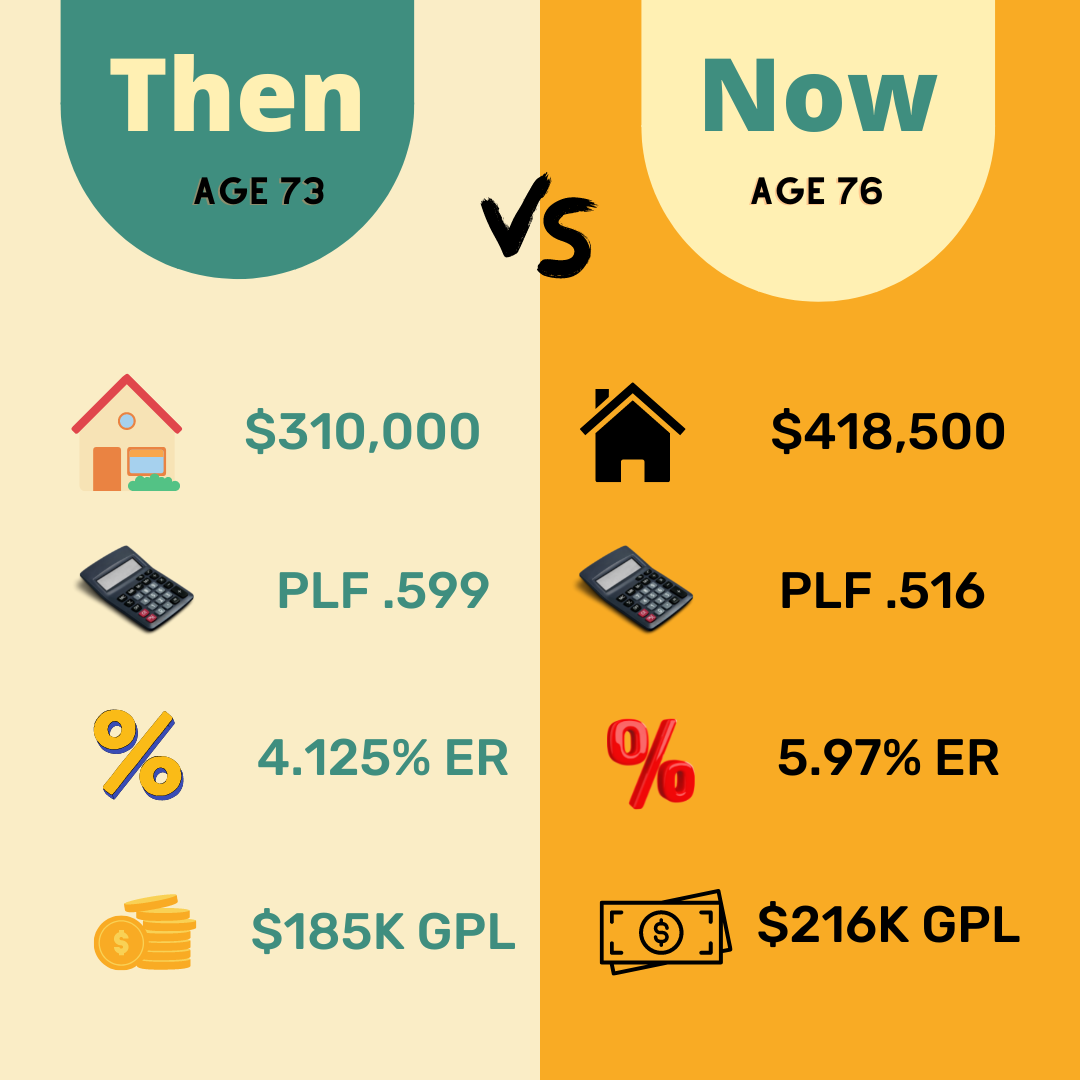

Exhibit 2: Take for example Ruth who was 73 years old in July 2019. At that time home was worth approximately $310,000 and her expected rate would have been 4.125%. This would have given her a gross principal limit (GPL) of $185,690.

Now fast forward to September 2022. Ruth may be three years older but she’s facing a much-higher expected interest rate of 5.87%. Is all hope lost? Far from it. While her PLF (principal limit factor) has dropped from .599 to .516 (a 14% reduction) her home value grew by 35% making her estimated home value $418,500. Consequently, regardless of today’s higher interest rates her gross principal limit grew from $185,690 in 2019 to $215,946. While Ruth did put off getting a reverse mortgage until three years later, she had the good fortune of pursuing the loan after a record surge in home values. This formula works even for homes that only appreciated 21% (versus the national average of 42%) during the same time period.

As a reverse mortgage professional now is the time to dive back into your old book of business, or your CRM. Here’s one suggested approach. Look for prospects you spoke with prior to 2021. Now add 30-40% to what their home was worth in 2019 or the typical appreciation rate in that market. Adjust for their current age and a slightly lower mortgage balance and run the calculation. Unless they refinanced their home and took cash out, many are likely to qualify. Even better, some who couldn’t qualify due to a high mortgage balance may qualify today thanks to their age, appreciated home value, and a few years of mortgage payments.

The impact of rising rates and lower principal limit factors cannot be denied. But neither can the mitigating factor of rising home values, for at least the present moment.

Additional reading:

[Yahoo Finance] FP Answers: My portfolio is down 30%. Do I still have enough to retire this year?

[/read]

No comment yet, add your voice below!